How rising prices, fragmented content, and platform aggregation are reshaping the streaming promise

When Netflix arrived in Australia in 2015, it was presented as a disruption. For years, Foxtel had defined subscription television with bundled packages, premium prices, and long-term contracts. Streaming promised something different: flexibility, affordability, and control. Watch what you want, when you want, without being locked in.

I have examined this shift and its longer-term effects on media industries and audiences in several of my writings on The Conversation.

Over a decade on, streaming is no longer just a challenger; it has become the dominant way Australians watch screen content. However, this shift raises an increasingly hard-to-ignore question: has streaming fundamentally changed the economics of television in Australia, or have we simply reconstructed the very system it aimed to challenge?

The Early Promise: Cheap, Simple, Different

In its early years, streaming felt almost too good to be true. Entry-level plans sat comfortably under $10 per month. Compared to Foxtel packages that could exceed $100, especially once sport was included. The value proposition was clear. It was not just about cost but also about control. One service could provide enough content for most households. Having two seemed like a luxury. The idea of maintaining five or six subscriptions at once would have appeared excessive.

The market, however, expanded rapidly. Stan entered alongside Netflix, followed by Amazon Prime Video, Disney+, Apple TV+, Kayo Sports, Binge, and Paramount+. Each offered exclusive libraries, original content, and in some cases, live sport. The outcome was not just more choice but also more division and fragmentation.

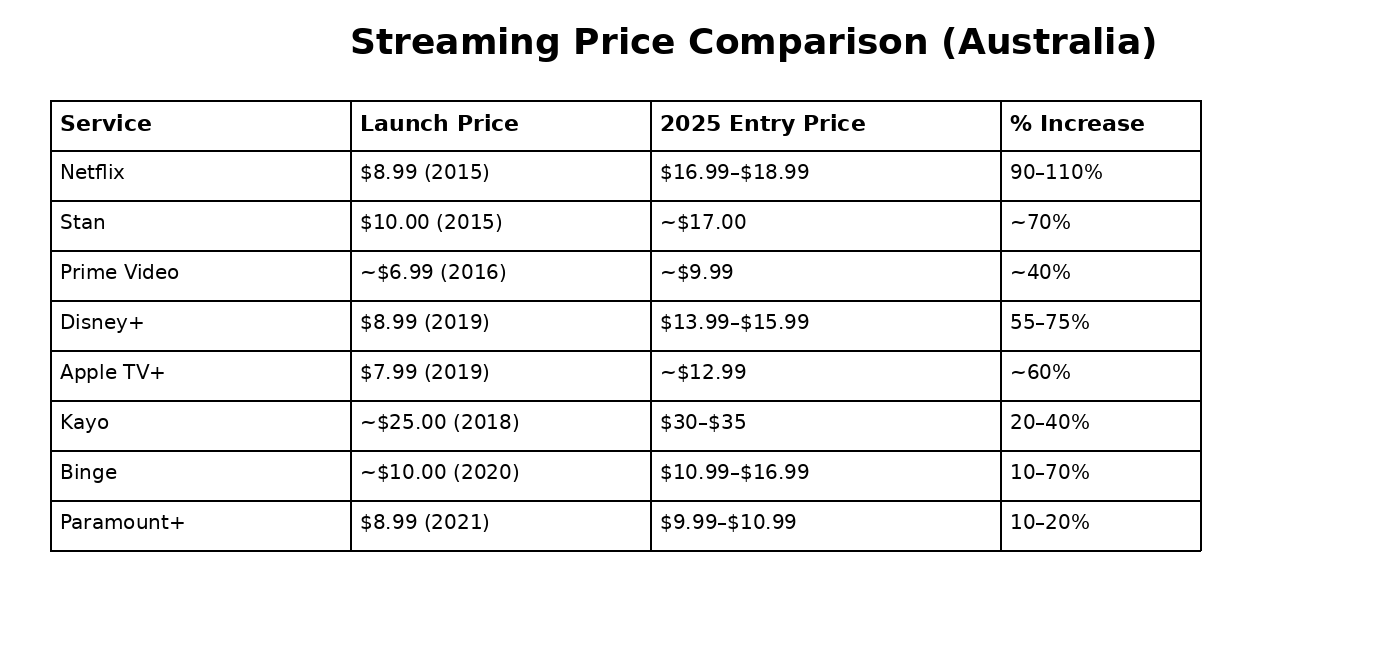

The Price Shift: A Decade of Increases

Over the past decade, the consistent rise in prices has become increasingly noticeable. Although each increase can be justified by factors such as higher production costs, competition for global rights, and the economics of original content, their combined impact is difficult to overlook.

These prices might seem reasonable on their own. However, the “entry price” often just serves as an initial access point. Many basic plans now have restrictions such as limited simultaneous screens, reduced streaming quality, or ads. For households, especially families, these restrictions are significant. To watch on multiple devices or to watch without ads, users often need to upgrade to higher-tier plans, which increases monthly expenses.

This is important to note, as streaming is no longer a single-service experience. A household subscribing to Netflix, Disney+, Stan, Prime Video, Apple TV+ and Kayo, at levels that meets their daily viewing needs, can easily spend over $100 each month. Include extra platforms or premium upgrades, and the total cost can match, or even surpass, the Foxtel packages many Australians originally wanted to avoid. Part of the reason Foxtel never got past a 30% penetration rate in Australian homes.

Fragmentation and the Return of the Bundle

Streaming promised liberation from the pay television bundle. Instead of paying for channels you never watched, you paid for access to the content you chose.

But that content is now distributed and fragmented across platforms.

- Want a major franchise? One service.

- Want a prestige drama? Another.

- Want live sport? Often somewhere else again.

Fragmentation has shifted from channels to platforms. In Australia, sport amplifies this trend, with rights divided among multiple providers. The outcome is not just more options but also greater complexity. Viewers are no longer using a program guide but navigating a subscription landscape, with no guide to help them find what they want.

The bundle did not disappear. It decentralised.

From Passive Viewing to Active Managing

This fragmentation has also reshaped audience behaviour. Streaming is no longer passive; it is now managed. Subscriptions are started and stopped in response to release cycles. Services rotate depending on content availability. Pricing announcements are closely watched. Essentially, audiences have become curators of their own access.

Meanwhile, platforms have matured. Features like ad-supported tiers, password-sharing limits, and tiered pricing show an industry shifting from quick growth to sustainable model. Streaming no longer aims to disrupt the system; instead, it now plays a role in maintaining it.

The Australian Context

Australia’s media landscape introduces another layer to this story. As a smaller market heavily reliant on US content and with a deeply rooted sports culture, the streaming scene is influenced by both international and local factors.

Local platforms like Stan and Binge have leaned into Australian content and sport to differentiate themselves, while global platforms carefully localise their offerings. The result is a market full of content but divided in access. For many households, watching broadly now means subscribing broadly.

Back to the Beginning? Or Something New?

The structure has shifted. Consumers now have more flexibility, more options, and more control than in the era of pay TV. However, from a cost perspective and increasingly from an access point of view, the experience can still feel familiar.

What is particularly revealing is how Foxtel has evolved over time. Instead of directly competing with streaming services, it now acts as an aggregator. Using its interface and devices, Foxtel combines multiple streaming platforms in an effort to create a single seamless environment, making it easier for users to find and access content across different services.

In a sense, this marks a return to a familiar approach. Instead of bundling channels like before, Foxtel now manages access. The interface acts as an organising layer over a fragmented ecosystem, aiding audiences in finding content across various platforms. This becomes more crucial as licensing agreements change frequently and content shifts between services over time. The challenge is no longer just paying for access, it is finding it.

Foxtel’s evolution indicates that while streaming has disrupted distribution, it has also brought in new kinds of complexity. Aggregation is developing as a way to manage that complexity, offering a solution to handle fragmentation without eliminating it.

This doesn’t mean we’ve simply gone back to the past. The system is more dispersed, and power is shared among various global and local players. However, the fundamental processes of bundling, aggregation, and layered costs are re-emerging in new forms.

A decade ago, streaming represented disruption. Today, it represents infrastructure.

Five Consideration Questions

- Has streaming genuinely reduced the long-term cost of television, or simply redistributed it across platforms?

- At what point does fragmentation stop feeling like choice and start feeling like complexity?

- How sustainable is a model where households must subscribe to multiple services to access mainstream content?

- Does aggregation solve fragmentation, or simply make it easier to navigate?

- If streaming has become infrastructure, what might the next true disruption look like?